If you’re a dedicated Apple enthusiast keeping a pulse on the latest tech developments, you’re likely aware of Apple’s recent foray into the finance sector with the launch of its proprietary credit card—the Apple Card.

The move comes at a strategic juncture for the tech giant, as iPhone sales have encountered a plateau in recent quarters.

While the concept of a credit card might seem unconventional for a company renowned for revolutionizing the smartphone industry, it proves to be a calculated move by Apple to solidify its relationship with existing customers and inject vitality into the revenue stream of its flagship product, the iPhone.

Not too long ago, during a special event, the Cupertino-based company unveiled plans to introduce a co-branded credit card in collaboration with financial powerhouse Goldman Sachs.

The juxtaposition of a company that reshaped the smartphone landscape with its groundbreaking iPhone now venturing into financial services is undeniably intriguing. The question on many minds is: What could possibly go wrong?

In this article, we’ll explain how Apple entered the finance industry and what it means for Apple and its user base. Let’s get started without delay because this article has a lot to cover.

The Back Story …

Over the years, Apple has reported inconsistent growth in iPhone sales during its quarterly earnings reports. When the company introduced the first iPhone, it was a major breakthrough in the smartphone industry.

People get excited every time a brand-new model comes out. As time passed, that hype began to fade away, as competition got tougher and new players like OnePlus and Huawei stepped up their games.

People will sign up for the Apple Card not because it’s the best credit card out there but because they love the brand.

If people don’t upgrade their iPhones as often as they used to, there’s a problem here for Apple from a profitability standpoint. Apple had to come up with different marketing strategies to boost its revenue.

The company started launching multiple iPhones per year, including a mid-tier iPhone, to reach emerging markets like China and India.

That didn’t really help; the iPhone 5R was a total failure, and the iPhone XR is probably on its way to repeating the same fiasco.

The majority of the company’s revenue comes from iPhone sales. In the third quarter of 2019, iPhone sales accounted for $25.99 billion out of a total revenue of $53.8 billion, marking the first instance since 2012 that iPhone sales constituted less than half of Apple’s earnings.

In the same optic of increasing revenue, the company introduced new paid services like the Apple News Plus and Arcade game earlier this year. By the way, in the near future, most of Apple’s revenue will come from Paid services.

iMessage, seamless integration between software and hardware, and top-notch customer service are among the obstacles that prevent iPhone users from switching to Android.

But iPhone and Android are now closer than ever, whether from a software or hardware perspective. It’s now easier to leave Apple without losing so much.

So, how does Apple keep current iPhone users?

How does Apple stop its loyal fans from leaving?

That’s what the Apple Card is for.

Let’s elaborate.

What Is an Apple Card?

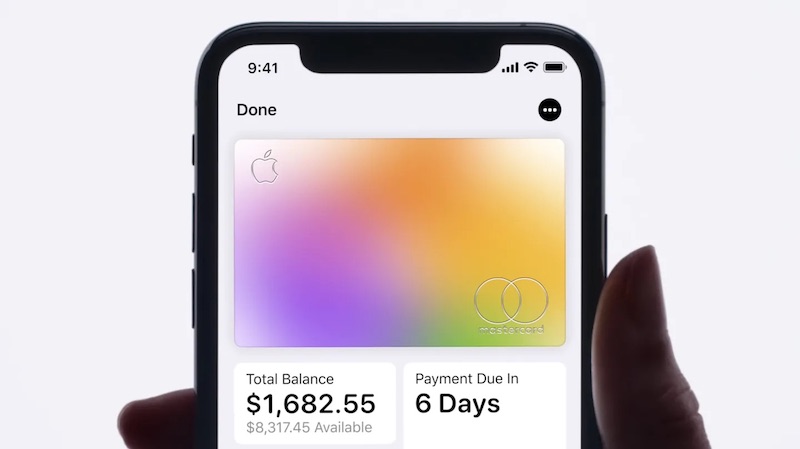

To put it short and sweet, Apple Card is a credit card that Apple created in partnership with Goldman Sachs, the Bank of the rich and powerful. Apple Pay is built into the Wallet app so you can use it for all your transactions.

Things get interesting here: you must own a compatible iPhone to apply for an Apple Card. It’s clear and simple: Apple Card is not for you if you don’t have an iPhone. Here are all the Apple Card requirements.

Why would Apple and Goldman Sachs release a jointly-branded credit card for only a selected market? Well, it’s typical for Apple to do whatever is necessary to keep its profits high.

First, the smartphone maker is not a credit card company and is not trying to compete against other credit card companies like Chase or Bank of America. Apple is in the business of selling iPhones and will continue to do so for many years to come.

Apple Card was introduced with the sole purpose of luring iPhone users into Apple’s ecosystem. It is a direct way for the company to counteract declining iPhone sales.

The Apple Card, crafted from titanium and adorned with laser-etched user names, distinguishes itself by the deliberate omission of numerical identifiers and expiration dates.

This design choice not only enhances a sense of exclusivity but also elevates the perceived uniqueness of iPhone users who utilize the card.

Apple launched the Apple Card just a month before its Fall iPhone Event, which is a great timing so people can have time to sign up for it and buy new iPhones.

We can deny it. The card has a clean and minimalist design, which is why most people will sign up for it. It’s sad, but that’s the reality of our society.

In general, metal credit cards are for the wealthy, and you can only get an Apple Card if you own an iPhone. This will play a key role in making iPhone users more loyal, which is critical for any business’ success.

Goldman Sachs, on the other hand, will attract customers (iPhone users) that it wouldn’t ordinarily attract.

However, declining growth and margins could be the company’s motivation. That’s also a great opportunity for Goldman Sachs to continue diversifying from a global investment bank to a consumer bank.

The card has no fees and the industry’s lowest interest rates with comparable cards. Credit card companies rely heavily on those fees and interests to make money. The winner here is Apple, big time.

Unsurprisingly, other banks that were in talks with Apple pulled out of the deal because of concerns about the product’s profitability. We’re not sure how this will play out for the Wall Street investment bank giant, but predictions are not good.

Treat Apple Card for What It Is

So, will iPhone users sign up for Apple Card? Absolutely yes. They’ll do it not because Apple Card is better than any other credit card in the market right now but because they love the brand. iPhone users will see it as another product launched by Apple, which is technically not.

The iPhone maker has been marketing the Apple Card as “a new kind of credit card made by Apple, not a bank.” Goldman Sachs is the bank that will lend you the money, not Apple, and they’re processing all the transactions.

Apple only provides the technology and tools to integrate the card seamlessly into your iPhone. Apple Card is just a credit card like any other credit card. Its cool new features, like tons of financial wellness tools, are designed to entice people and make it look like something totally new to the industry.

Don’t get me wrong. Those tools are super useful and nice to have. Having these features on every credit card is a good idea, but don’t let that detract from the main reason Apple designed the Apple Card in the first place.

Now, how will Apple Card lock down iPhone users into Apple’s ecosystem?

If you have already signed up for an Apple Card, you should know it will have massive implications for your financial life. Let me explain what I mean by this.

While Apple claims the Apple Card represents everything the company stands for, including privacy, security, and simplicity, you should know Goldman Sachs has been involved in controversies and legal disputes worldwide. So you know who you’re doing business with.

I’m not sure why Apple would choose Goldman Sachs as the issuing bank, given its bad reputation for doing business. This deal should be an eye-opening warning to all iPhone users.

Let’s say you already own an iPhone and are considering signing up for an Apple Card. The process is super quick. You can approve it in seconds and start using it immediately.

The Apple Card gives you an advantage over most credit card applications, which usually take days from when you apply to when you receive the card and can begin using it.

According to the Federal Reserve, US credit card debt hit $1.04 trillion, the largest ever.

Keep in mind there’s no sign-up bonus for this card. A discount on your next iPhone purchase would be logical, not even an AirPods. The only incentive you get is the Apple logo on the card. It’s Apple. Their greed for money knows no bounds.

Now that you have your sleek rectangular titanium, what do you do next? You start using it for everyday small expenses and will buy the next iPhone and Apple Watch with it, which is Apple’s ultimate goal. That way, credit card debt will continue to hit record highs. Let’s put that into context for a moment.

Remember Who You Do Business With

Apple Card is intended for millennial borrowers who love but cannot afford Apple products. People will buy a product they cannot afford with a credit card co-created by the same company selling those products, which is a double win for Apple.

The best analogy is that the company kills two birds with one stone. If you think Apple was good at making money, wait for its next quarterly earnings report and follow its stock closely. The giant tech will make ridiculous money from you buying its expensive products with the Apple Card.

Now that you’re locked down even more in Apple’s ecosystem. How do you get out?

Let’s say you finally realize that you can live without iMessage because there are actually plenty of great messaging apps out there. Let’s say you want to buy a new, more affordable smartphone and suddenly find yourself in a tough situation.

Your Apple Card is tied to your iPhone, so you won’t be able to use it anymore. You have no choice but to close that credit card, which might have massive implications for your credit history. That’d be something you don’t want.

Now it looks like Apple Card is all evil. Absolutely not. This card is for you if you’re a die-hard Apple fan and can afford its products.

But you’re probably not the ideal customer of Goldman Sachs since you’ll be able to pay off your balance every month. Therefore, they’ll make no money off of you.

It’s no surprise to anyone that people with subprime credit scores are getting approved for the Apple Card. That’s the kind of customer Goldman Sachs targets, and you should be very careful if you fall into that category.

Goldman Sachs will rip Millennials off with the “no late fees” card. It’s already hard for most people to keep up with their credit card payments on time, so imagine having a card with no late fee penalty.

Bingo! Dream comes true. Not so fast. You’ll end up paying massive interest on that balance you carry on a monthly basis, and it will be much harder to get out of this debt cycle.

Wrap-Up: Is Apple Card Worth It?

Now, over to you.

Are you considering signing up for the Apple Card?

Are you concerned that Apple has partnered with Goldman Sachs to create a co-branded credit card?

Either way, let us know your thoughts in the comment section below.